Optimism returns: WoodMac calls for $450 billion in upstream O&G project FIDs in 2017

According to Wood Mackenzie’s global upstream outlook for 2017, confidence will start to return to the oil and gas sector in 2017, with exploration and production spend set to rise by 3% to US$450 billion.

The investment level is still 40% below the heady days of 2014, the group points out.

At the forefront of the revival will be U.S. tight oil. Costs will continue to fall in 2017, though only marginally.

U.S. tight oil, and the Permian basin in particular, will lead the way, distinguished by low breakevens, scale and flexibility. U.S. Lower 48 spend is set to grow by 23%, to U.S. $61 billion, with upside if oil prices rise strongly and U.S. Independents are emboldened by a Trump presidency.

“Nowhere is the mantra ‘doing more with less’ more evident than onshore U.S. There has been a dramatic increase in efficiency in the sector, exemplified by the drillers, who are managing to complete wells up to 30% quicker,” Dickson said.

Wood Mackenzie says as the tight oil sector heats up, the spectre of cost inflation looms in 2017. But any increase in costs may well be offset by further efficiency gains in earlier-life plays. For example, there’s still potential for a further improvement in drilling speed of 20% to 30% in some early-life tight oil plays.

A much leaner industry: CapEx per barrel in 2017 shrinks to $7 from 2014’s $17

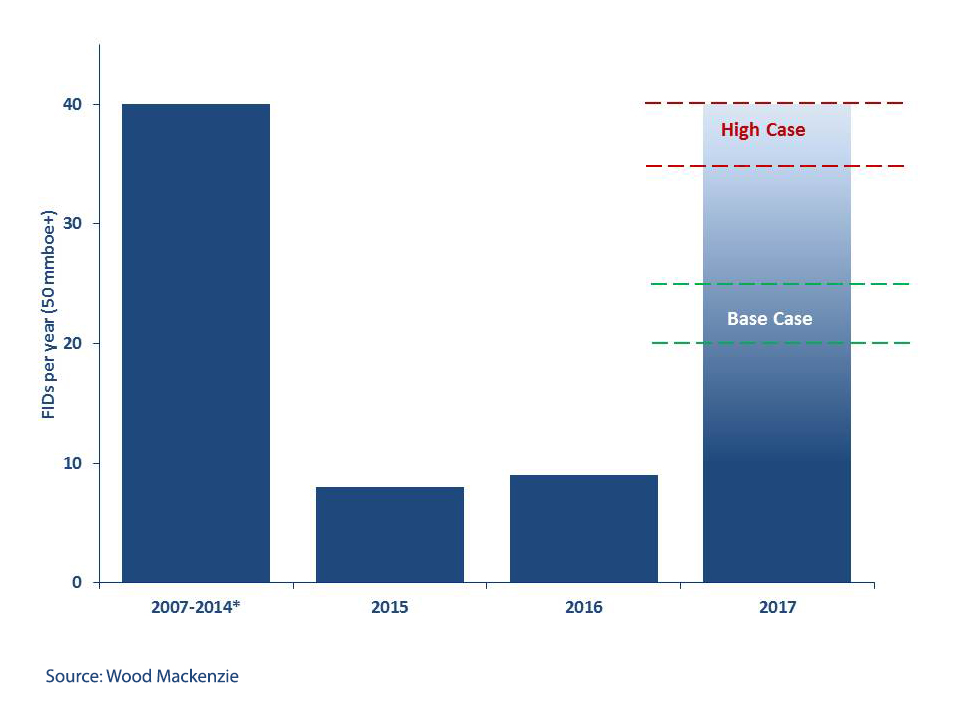

Wood Mackenzie predicts the number of FIDs will rise to more than 20 in 2017, compared with nine in 2016. This is still well short of the 2010-2014 average of 40 a year. But these are generally smaller, more efficient projects, and capex per barrel of oil equivalent (boe) averages just US$7 per barrel, down from US$17 per barrel for the 2014 projects, the consultancy said.

“Companies will get more bang for their buck as development incremental internal rates of return (IRR) will jump from 9% to 16%, comparing 2014 to 2017,” said WoodMac E&P analyst Malcolm Dickson. “This is in part a result of a shift in capital allocation away from complex mega projects towards smaller, incremental projects in the Canadian oil sands and deep water.”...MORE

CHART BELOW: FIDs per year: 2007-2017 (Greater than 50 mmboe)